Creating a Budget That Actually Works

Step-by-step approach to building a realistic monthly budget. Most people spend too much time on budgeting tools and not enough time on the actual numbers that matter.

Read MoreVague goals don’t work. We’ll walk you through making goals specific enough to actually achieve—whether it’s saving for a home, education, or retirement.

You’ve probably set financial goals before. Save more. Pay off debt. Build wealth. Sound familiar? Here’s the thing—goals like these almost never stick. They’re too vague. They don’t give you anything concrete to work toward.

The problem isn’t a lack of motivation. It’s that you can’t measure progress on something that’s not clearly defined. Without clear targets, it’s impossible to know if you’re actually moving forward. This is where most people get stuck.

We’re going to change that. By the end of this guide, you’ll know exactly how to set financial goals that actually work. Goals that are specific enough to track, realistic enough to achieve, and important enough to matter.

You’ve probably heard of SMART goals. Specific, Measurable, Achievable, Relevant, Time-bound. It sounds corporate, but it’s actually the most reliable way to set goals that stick. The reason? It removes all the guesswork.

Let’s break this down with real examples. Instead of “save more money,” a SMART goal looks like: “Save RM500 every month for the next 24 months to build an emergency fund of RM12,000.” Suddenly you’ve got a number. A deadline. A clear reason why. That’s the difference between a wish and a plan.

The framework forces you to think through the details. And details are what make goals real.

Setting a goal takes maybe 15 minutes. Making it stick takes a bit more thought. Here’s the process we recommend.

Before you set a goal, you need to know your current situation. How much are you earning? What’re your monthly expenses? How much debt do you have? This isn’t about judgment—it’s about having real numbers to work with. Spend an hour going through your bank statements. Write down the actual numbers. This baseline is everything.

Don’t set a goal because you think you should. Set it because it actually matters to your life. Want to buy a house? Great. Want to send your kids to university? Solid goal. Want to have three months of expenses saved up? That’s a real emergency fund. The goal needs to connect to something you actually care about. That’s what makes you stick with it when it gets boring.

A goal of “save RM50,000 in five years” can feel overwhelming. But “save RM833 per month” is doable. It’s something you can check off every 30 days. The smaller milestones give you wins along the way. You’ll see progress. You’ll stay motivated. That matters more than you’d think.

Here’s how the framework applies to the goals most people actually want to achieve. Use these as templates for your own.

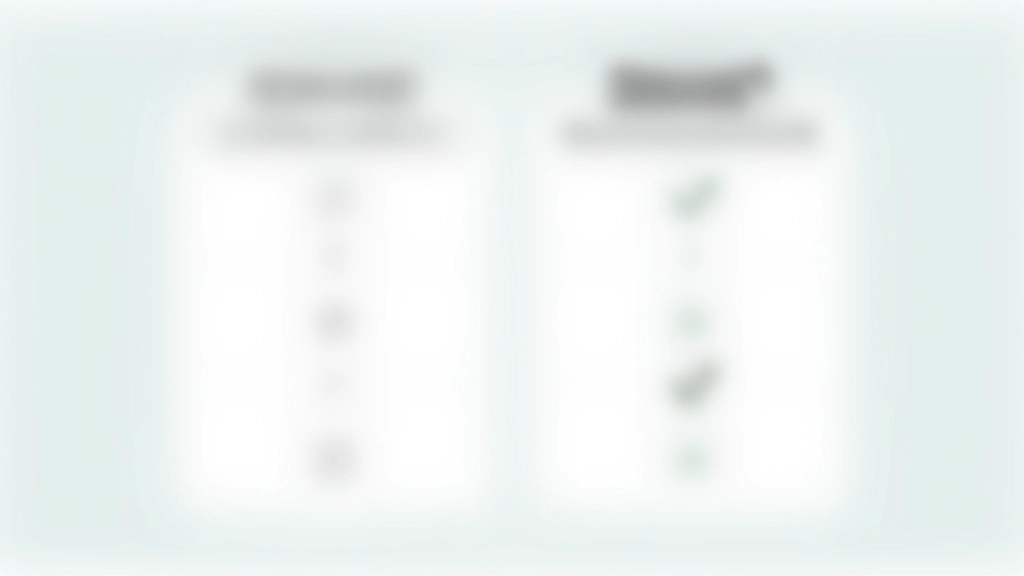

Vague: “Build an emergency fund”

SMART: “Save RM500 every month for 18 months to build a RM9,000 emergency fund (covering three months of essential expenses)”

Vague: “Save for a house down payment”

SMART: “Save RM1,200 monthly for 60 months to accumulate RM72,000 for a house down payment by December 2030”

Vague: “Save for kids’ education”

SMART: “Contribute RM400 monthly to an education fund for four years, targeting RM19,200 for first child’s university costs”

Vague: “Pay off credit card debt”

SMART: “Pay an extra RM300 toward credit card debt monthly to eliminate RM8,500 balance within 24 months”

Setting the goal is half the work. The other half is keeping track of it. Without tracking, goals disappear. You forget about them. Then a year passes and you realize you haven’t moved forward at all.

Here’s what works: Pick one simple way to track. Could be a spreadsheet. Could be a notes app. Could be a physical notebook. Doesn’t matter. What matters is that you review it monthly. Every month, check your progress against the target. Are you on track? Ahead? Behind? Know where you stand.

When you see the numbers go up month after month, it creates momentum. You’ll feel the progress. That feeling is what keeps you going when motivation dips. And it will dip—that’s normal. But if you can see the numbers moving, you’ll push through.

The difference between a goal that works and one that doesn’t isn’t motivation. It’s specificity. When you know exactly what you’re saving, how much, and when you need it by—you’ve got something real to work toward. That clarity is what turns a wish into a plan.

Take 30 minutes this week. Write down one financial goal using the SMART framework. Get specific. Put numbers on it. Give it a deadline. Then pick your tracking method. That’s it. You’re not doing anything complicated. You’re just being clear about what you want and how you’ll measure progress.

Financial goals don’t fail because people lack discipline. They fail because the goals themselves are too fuzzy. Fix that, and everything changes.

This article is educational in nature and intended to help you understand the principles of goal-setting for personal finances. It’s not financial advice, and circumstances vary for every individual. Consider consulting with a qualified financial advisor who understands your specific situation before making major financial decisions. The examples provided are for illustration purposes and may not reflect your personal financial reality or local market conditions in Malaysia.

Step-by-step approach to building a realistic monthly budget. Most people spend too much time on budgeting tools and not enough time on the actual numbers that matter.

Read More

How much should you save? Where should it go? We break down the logic behind emergency funds and how to build one without sacrificing your other goals.

Read More

Interest rates, minimum balances, withdrawal limits. We’ve looked at what Malaysian banks actually offer and what features you should care about most.

Read More